How Financial Services Institutions Can Nail Their Content Marketing Strategy

A content marketing strategy gives financial institutions a competitive edge that paid advertising budgets alone can’t match, especially for small to mid-sized banks and credit unions going up against national players. Building one requires four phases: defining your goals and audience (blueprint), selecting formats and distribution channels (foundation), producing content pillars and planning calendars (build), and setting up reporting that ties back to business outcomes (report and refine). When these phases work together, content becomes a system that attracts customers, retains existing ones, and positions the institution as a trusted financial resource in the community.

The level of effort that financial institutions place on developing engaging content has sky-rocketed in recent years. This isn’t surprising, given that an effective content strategy can help attract new customers and retain existing ones. It also serves as an opportunity to educate your community on financial matters.

But with so many institutions taking this approach, what sets the winners apart from the losers? The most successful content marketers in the financial industry have one thing in common — a great strategic foundation for their content. They know who they are. They know who their desired customers are, and they develop their marketing content strategy around answering their customers’ questions. This differentiator can be particularly important for small to mid-sized institutions. This is because they’re better equipped to invest in developing a content strategy that rivals a large national institution. They are less able to match the funds required to compete with megabanks on paid advertising campaigns. In other words, a great content strategy can be a field-leveler when a smaller institution is going toe-to-toe with Goliath for market share.

Conversely, content marketing without a content strategy can be like having a high net income but no financial plan.

What Is the Purpose of a Content Marketing Strategy?

First, we have to define content marketing and define how it is different than marketing content. Michael Brenner first addressed this in 2016 in a Content Marketing Institute article and has since been quoted countless times:

- Content marketing is about attracting an audience to an experience (or “destination”) you own, build, and optimize to achieve your marketing objectives.

- Content is everywhere. There’s product content, sales content, customer-service content, event content, employee-generated content, marketing and campaign content. Even advertising is content.

- With content marketing, you are attracting an audience to a brand-owned destination versus interrupting or buying an audience on someone else’s platform.

- Content marketing can take on many different forms.

Bringing more value to communications

Organizations integrate content marketing into their marketing mix for various reasons. The main goal is to be less “salesy” and demonstrate greater value in their communications. In doing so, they:

- Establish subject expertise

- Differentiate themselves as being local or tied to the community

- Dig down deep on a specific issue loosely relevant to the whole audience bus specific to a few

- Elevate and expand their Q&A section/content

- Improve their SEO significantly, if done deliberately

- Engage teammates tasked with the development of content

- Step back from content tactics to visualize the big picture of how all of their content efforts are working together

Involving different stakeholders at different phases of the content creation process can lead to better cross-functional and cross-departmental cooperation. Mortgage brokers, financial planners, and other members are called in as experts to work closely with marketing to write and publish relevant professional content. This can also lead to cost savings as often engaging current employees allows for an organization to rely less on agencies and other outside sources.

How institutions prioritize will be different from organization to organization depending on their goals, industry, resources, and competitive landscape. Gaining internal alignment on the direction of your content can be one of the biggest positives of developing a content strategy, as it allows all contributors to understand how their role is part of a bigger picture.

What Should Be Included in a Content Marketing Strategy for Financial Services?

There’s no hard and fast rule for what to include in a content marketing strategy. The content should reflect the individual organization’s purpose and goals for developing content in the first place, as well as the needs of their desired customers. That said, quite a few common components are included in content marketing strategies fairly frequently.

For the purpose of organization, we will compartmentalize these components into phases, which we’re referring to as the following:

- The blueprint phase

- The foundation phase

- The build phase

- The report and refine phase

1. The blueprint phase

These phases aren’t ubiquitously recognized parts of a content strategy but simply serve as a way to organize some of the most common inclusions.

This phase is where you define what you’re trying to achieve and seek to gain internal alignment on your direction prior to executing further work. Some common aspects to include in this phase are as follows.

Brand Voice

The development of a brand voice isn’t necessarily an activity of content marketing strategy. That’s because most organizations will have conducted a brand identity exercise that includes brand voice prior to developing a content strategy. This scenario is ideal. Regardless of whether your brand voice already exists or is being developed as part of your content strategy, it should be included in the strategy document to guide those creating content.

Audience Insights

The table stakes for this include a list of target audiences with a few key data points for each audience. A strong approach to audience strategy goes a lot deeper than this, though. Psychographic and media consumption data by audience segment can help you refine how you will reach each audience segment and determine what messaging will appeal to them. The development of personas can help take this a step further and bring the target audience to life. Once you have a clear perspective of your various target audience segments, it can be a useful exercise to cross-tabulate key differences and similarities across the segments.

Objectives and KPIs

When working with an agency, this should always be a collaborative process. There typically are a couple of precursors to developing detailed objectives and Key Performance Indicators (KPIs). First, there should be alignment regarding the purpose of the content efforts. This alignment should be present between all applicable departments/stakeholders at the institution as well as between the institution and its agency. From that should come the business goal(s) of your content marketing efforts. Once you’ve decided why you’re doing it and what impact you want it to make on the business, it’s time to map out what measurable objectives and KPIs you will monitor to prove efficacy. KPIs should be specific, achievable, and measurable (SAM) and, as such, will allow you to monitor progress throughout the marketing efforts to see how you’re tracking toward your objectives.

2. The foundation phase

Now, it’s time to think through the mechanics and processes of your plan prior to beginning content planning. Consider the following elements at this point:

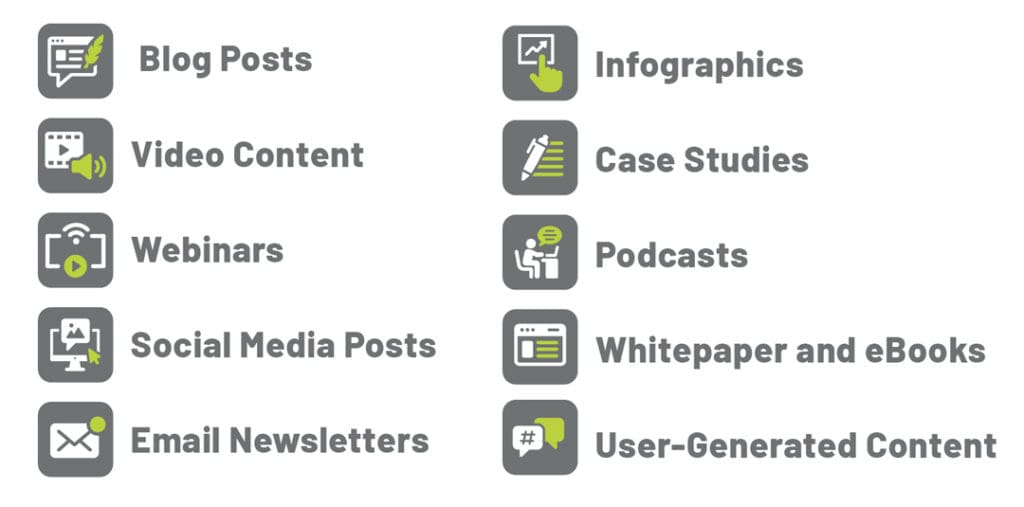

Content formats

If you included media consumption habits as part of your audience insights, then that information should allow you to easily decide what formats are going to be most appealing and accessible to your audience. Granted, not all content requires the same level of resources to develop, so it’s important to be realistic about what you can support. A third consideration when thinking about formats beyond effectiveness with the target audience and the cost/effort required for development is how versatile a particular format is. There might be cases where a video isn’t the lightest content lift. Still, you know you could use a short video on an important topic in multiple places, where a cheaper social media graphic might be easier but far less engaging and useful. In a case like this, penny-wise may be pound-foolish.

Distribution channels

There’s a significant relationship between content formats and distribution channels as the two are intertwined in a way that makes it most practical for marketers to think through both questions simultaneously. Putting distribution channels first would cause marketers to select the channels that will result in the best reach regardless of whether the format is a good fit for your objectives or requires a substantial amount of effort to implement. However, not thinking about channels until you’ve made final decisions on format could cause you to miss out on reaching a considerable portion of your target audience.

Cross-pollination considerations

Considering cross-pollination at this time rather than later is prudent. An obvious output is that it allows you to make maximum use of any piece of content you develop. A less obvious perk is that considering this early on can help with format selection. It allows you to choose a mix of formats that align with your audience’s preferences and support content cross-pollination.

SEO strategy and keywords

The importance of this item depends heavily on where you net out regarding content formats and distribution. SEO is critical at this phase if your distribution involves any owned resources (i.e., publishing to a blog on your own website). You wouldn’t include SEO in a content strategy focused solely on earned and paid tactics. However, insights from the SEO strategy and keyword recommendations can often inform your approach to certain earned and paid tactics.

3. The build phase

This phase is less about building out the final content and more about producing the components of your content machine. Doing a thorough job in this phase offers many benefits to financial institutions. It makes the content development process go much more efficiently. Still, more importantly, readers can see the intentionality of content when there’s a steady stream of thoughtful content pieces that seamlessly synch up with one another. Banks and credit unions can consider a lot of elements to put into this phase, but below are some of the most critical components:

Content pillars

Having established pillars and a set monthly target for the amount of content within each pillar can make content creation more efficient while also adding parameters to the process. It also helps ensure that there isn’t a pillar that goes neglected for too long of a period.

Content planning

How far this is taken varies. However, a good place to start after you have content pillars is to build out content for at least the first full month. Beyond that, you should at least have a list of content ideas for the following month. The format of this can take different forms, but we find that a visual calendarized view tends to be most helpful. It’s important to be able to show all relevant communication channels in the same view so that you can consider how all of your outreach is working together.

Managing your database

With any traditional inbound strategy, the content nurtures leads into customers and customers into repeat customers through constant presence and awareness. That way, when the time is right, the company is in the consideration set. Lead nurturing through sending personal emails to your database should also be part of a successful content marketing build. While additional content like promotional offers can be sent via the database, the pertinent, informative content is foundational.

Paid promotion plan

Not all content strategies require paid support, but they should always be considered and aligned prior to launching content. A smart paid promotion strategy can help get your content in front of a larger audience than organic promotion alone. Some audience subsets view self-help resources much more favorably than paid promotion of products or services. Effective alignment between content and intended audience can drive much greater conversion success, and digital media is a great means to serve tailored messaging to just the right audience.

Social media integration

While promoting your content marketing via your social media shouldn’t be your only social media effort, it should be a significant part. Promote and tease content articles, videos, and more across each social media platform in a way that feels natural to the platform. As we discussed in an earlier article, social video will eclipse linear TV in ad spend in 2025. Also, consider boosting posts promoting your content. Paying influencers to collaborate on posts promoting your content can also be helpful.

4. The report and refine phase

As with the build phase, this phase concerns planning for the subject at hand versus implementing it. The fact that reporting is backward-looking is not an excuse to not think about it until it’s time to produce a report. Having a solid plan ahead of time determines exactly how, when, and what to report.

This is also the time to reflect on the blueprint phase and reevaluate your objectives and KPIs. It’s imperative to ensure that your reporting strategy, cadence and technical setup all support the action of meaningfully reporting against your objectives. If you plan to use a dashboard for reporting, it’s important to get it set up prior to disseminating any content so that you can see data begin to populate as soon as the efforts launch.

The purpose of reports

Another very important consideration at this phase is to think through what the purpose is of any reports you plan to implement. You may find that you need to shift your reporting strategy if it doesn’t align with the purpose. For instance, imagine your report has a dual purpose: proving ROI and optimizing your marketing efforts. However, by the time you have hard ROI data, the opportunity to optimize is gone. This would make it safe to say you need two reports instead of one. A marketing report that’s lean, agile, and at least somewhat self-populating, along with an ROI report that factors in sales data but is only pulled quarterly or less.

Many CRMs, when set up properly, can manage databases and track social media and most digital media. They can also identify leads in your database, track their activities on your website, and enable marketing automation.

Thinking through these factors and putting a plan on paper will help ensure that not only your reporting efforts are accurate and timely but also that the takeaways are actionable in a way that moves the needle on your marketing efforts.

Time To Start Planning

We’ve covered the basic elements to consider in a content marketing strategy, but the best strategies actively capture what makes the marketer special. What’s in their DNA that sets them apart in a competitive marketplace? These aren’t questions you need to answer as part of the content strategy; they’re questions you should already know the answer to. However, you should be asking these questions while developing the plan because the plan itself needs to evoke those brand characteristics.

If you would like the support of an agency partner in taking you through this process, or if you need help setting your strategic foundation prior to taking on a content marketing strategy, give us a call at 502-499-4209 or drop us a note online.

KEY TAKEAWAYS

- Content marketing can level the playing field for smaller financial institutions that can’t match megabank ad budgets.

- A brand voice, audience insights with psychographic data, and clearly defined KPIs should all be established before any content gets created.

- Format and distribution decisions should be made together, since the two are deeply connected; choosing one without the other leads to misalignment.

- SEO strategy belongs in the planning phase if any content will live on owned channels like a blog or website.

- Content pillars with monthly targets keep production consistent and prevent any one topic from being neglected.

- Reporting needs its own plan before launch, including whether you need separate reports for optimization (fast, lean) and ROI (quarterly, sales-integrated).

Our Articles Delivered

Signup to receive our latest articles right in your inbox.